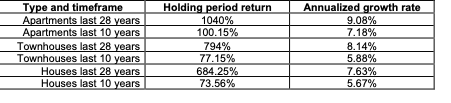

The Fund’s focus market is the city of Oslo in Norway.

Below you will find a brief overview of the market characteristics and why we believe we have a high potential to make an impact.

We believe that this is a long term trend.

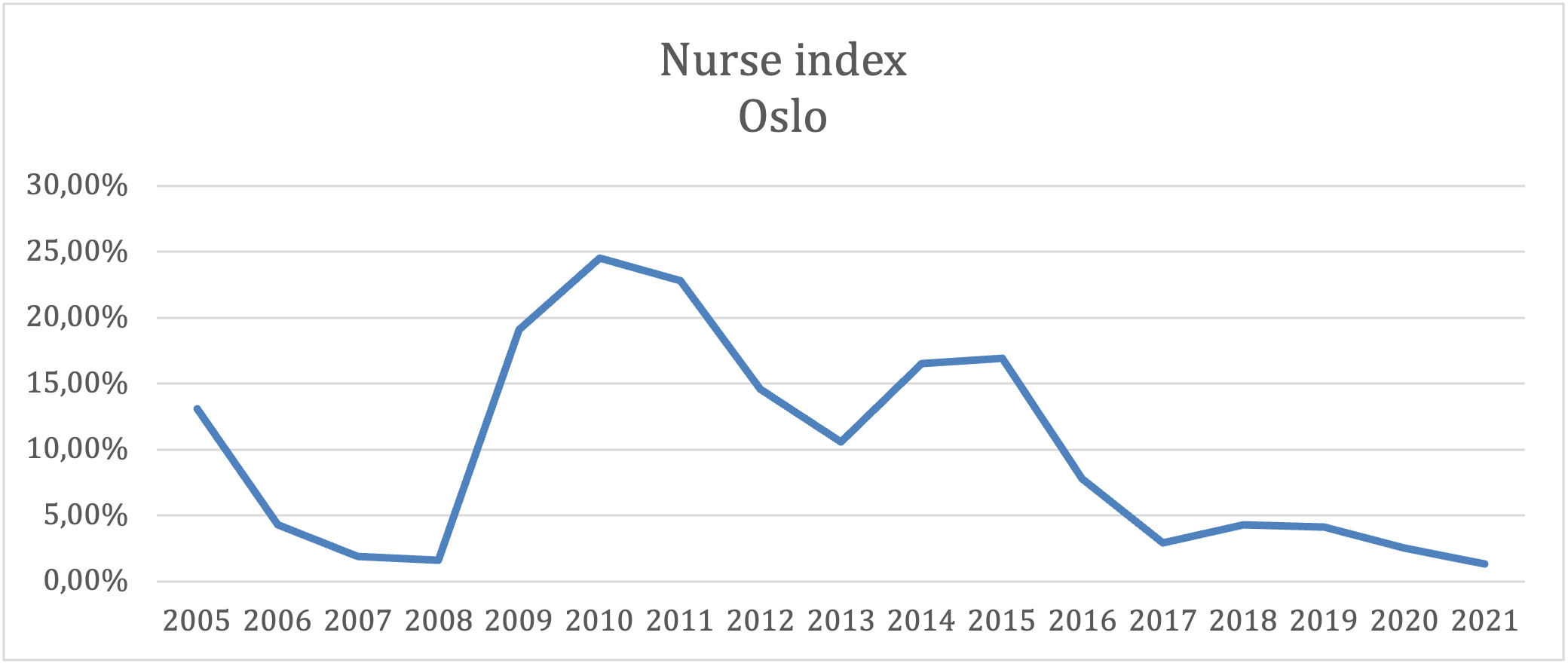

The nurse index measures how large a share of the sold homes a single nurse receives financing to buy. If the nurse can buy a high proportion of the homes in a city, housing prices in the city are low. If the nurse cannot buy any of the homes in a city, it is problematically expensive. The index has been prepared for some selected cities in Norway over time. The nursing profession is suitable because the income represents a typically good Norwegian income, and is to a small extent cyclical. The vast majority of home buyers in Norway finance home purchases by taking out a mortgage.

In Oslo the Nurse index has developed from 13% in 2005 to 1.3% in 2021 pictured in the chart below. That means that a nurse, or a person with an average good salary, savings of NOK 450,000 and a cheap student loan of up to NOK 200,000 can afford only 1.3% of homes in Oslo in 2021. This demonstrates that housing affordability has been on a decline since 2009.

Norway is an attractive place to live in. The migration to Norway and in this case to Oslo has been net positive the last decades. The population of Oslo has increased from 508,726 inhabitants in 2001 to 599,230 in 2011 and 697,010 in 2021. That is 37% growth since 2001 and 16.3% growth since 2011. The annual average net growth in population is 1.5%. Our target customer base for the Fund are millennials, in particular the population between 24 and 40 years old. Total millennial population is around 207,892 in Oslo in 2020, or almost 30%.

Targeted Co-owner profile for the Fund is the millennial generation aged between 25-40. They are first – or second time buyers of residential real estate and need help with equity down payment to obtain a mortgage for financing the purchase. They have regular income and a healthy economy, and the ability to obtain and service a mortgage loan from a bank. They should be able to demonstrate that they understand entirely the Co-ownership Agreement with the Fund.

Total market turnover in residential property in Norway was NOK 398B in 2020 (excluding off-plans). The number of first time buyers in Norway are also increasing, and 2020 reported the highest number of first time buyers since 2011 with 54.000 new homeowners.

Private debt is estimated to be rising further as housing prices increase and the population keep both buying new properties and refinancing their existing properties at higher valuations. This magnifies the problem the Fund is solving.

With an average price of NOK 4,247,937, the total market for the first time buyers is approximately NOK 229B. In Oslo, 11,413 people bought their first home in 2020 which is slightly above the average for the last 10 years. With an average price in Oslo of NOK 6,132,332, where first time buyers are unlikely purchasing at the average price, we estimate a market turnover range for our target customer group between NOK 46 and 69B.Hence,15% of the equity down payment requirement accounts for a market range of 6.9B and 10.4B. This range is the Fund's impact field in Oslo each year.

The systematic risk on private individuals is relatively low in Norway. The default rate of private households on loans has declined from around 5% in the early 1990´s to 0.4% in 2019 (Statistics Norway). The average default rate over the last 10 years is 0.56%. It is worth mentioning that the private debt-to-income ratio in Norway has been on a constant increase last decades, from 1.33 in 2000 to 2 in 2010 to 2.44 in Q2 2021.[3] It is estimated to be rising further as housing prices increase and the population keep both buying new properties and refinancing their existing properties at higher valuations as predicted by Sparebank 1 Markets.[4] This magnifies the problem the Fund is solving and the need for equity financing in general.

[1] https://www.ssb.no/en/priser-og-prisindekser/boligpriser-og-boligprisindekser

[2] https://eiendomnorge.no/aktuelt/blogg/sykepleierindeksen-h1-2021

[3] https://www.ssb.no/nasjonalregnskap-og-konjunkturer/faktaside/norsk-okonomi

[4] https://e24.no/norsk-oekonomi/i/AlG4ej/nordmenns-rekordgjeld-kan-bli-enda-stoerre-fremover-risikoen-er-hoey